WASHINGTON, Jan 24 (Reuters) - The Federal Reserve may not raise interest rates until March, but officials' tougher language about inflation is already kicking in, with borrowing costs rising for everyone from homebuyers to the federal government and stock markets kicking off the year deep in the red.

The pace of that adjustment now poses an unexpectedly urgent question for U.S. central bank officials at their latest two-day policy meeting this week: Are financial markets tightening too fast for what the Fed intends in its inflation battle, or is the Fed the one underestimating what will ultimately be needed to slow the pace of price increases?

In their most recent projections, issued in December, policymakers said they expected as many as three quarter-percentage-point rate increases this year, with more in the cards in 2023 and 2024. But those projections never raise the Fed's benchmark overnight interest rate above the "neutral" level that would actually restrict the economy.

Register now for FREE unlimited access to Reuters.com

Yet inflation still falls, a best-of-all-worlds outcome some analysts see as unrealistic.

"The U.S. is facing the highest inflation since 1982 and there is compelling evidence that a good chunk of it will persist. The Fed has never responded this slowly ... and even today is signaling a benign hiking cycle," wrote Ethan Harris, the head of global research at Bank of America. "The biggest near-term risk is right in front of us: that the Fed is seriously behind the curve and has to get serious."

That could mean as many as six quarter-percentage point rate increases this year, he said, and a fast push to a 3% federal funds rate from the current level near zero. That'd be the highest policy rate since the Fed started slashing borrowing costs at the start of the 2007-2009 financial crisis, and enough, according to current estimates, to actually curb economic growth, employment and inflation.

In the Fed's current projections they merely do less to prop it up.

Fed officials won't update their formal outlook at the Jan. 25-26 policy meeting. But Fed Chair Jerome Powell will hold a news conference after the release of the policy statement on Wednesday to talk in more detail about the Fed's plans, the current view of the economy, and the recent resetting of rates and equity values. That has included a more than 7% decline in the S&P 500 (.SPX) index since Dec. 31.

'SHADOW' RATE HIKES

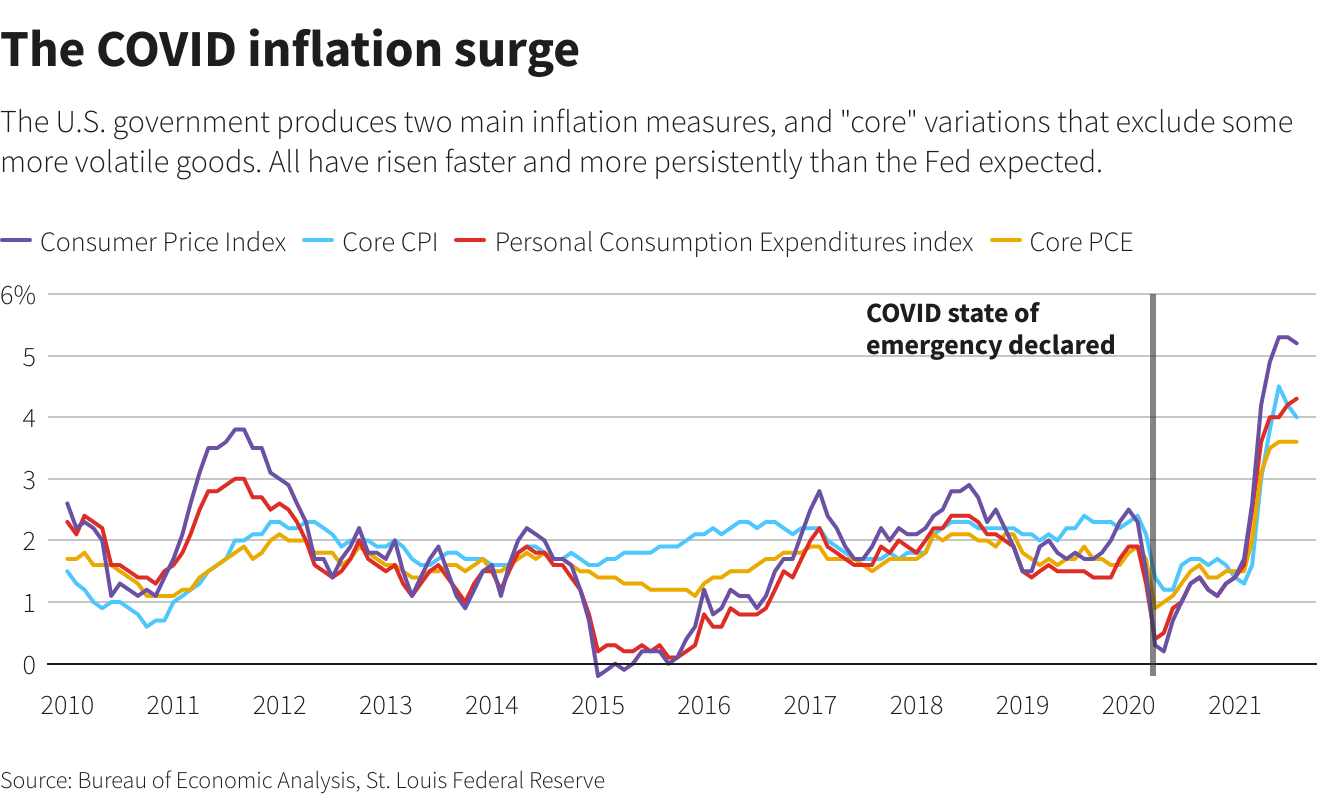

For a central bank that just a few months ago still promised open-ended support until the economy was fully healed from the coronavirus pandemic, the surge in U.S. inflation to a 40-year high kickstarted a high-stakes policy shift away from pandemic support.

A "liftoff" of interest rates has been flagged for March, years ahead of what was thought likely at the start of the health crisis. At the same time, the Fed is planning to shrink its holdings of U.S. Treasury bonds and mortgage-backed securities - using a second lever to ratchet up the cost of credit.

How the two policy tools interact remains a topic of analysis and debate - as does the eventual influence on inflation, the variable the Fed ultimately is trying to control.

Even with three rate increases and a smaller balance sheet in the offing, investors so far are assuming the Fed will have to do more to bring price increases back into line with its 2% inflation target. Trading in futures contracts linked to the federal funds rate shows four rate increases expected this year, for example, and is edging towards five.

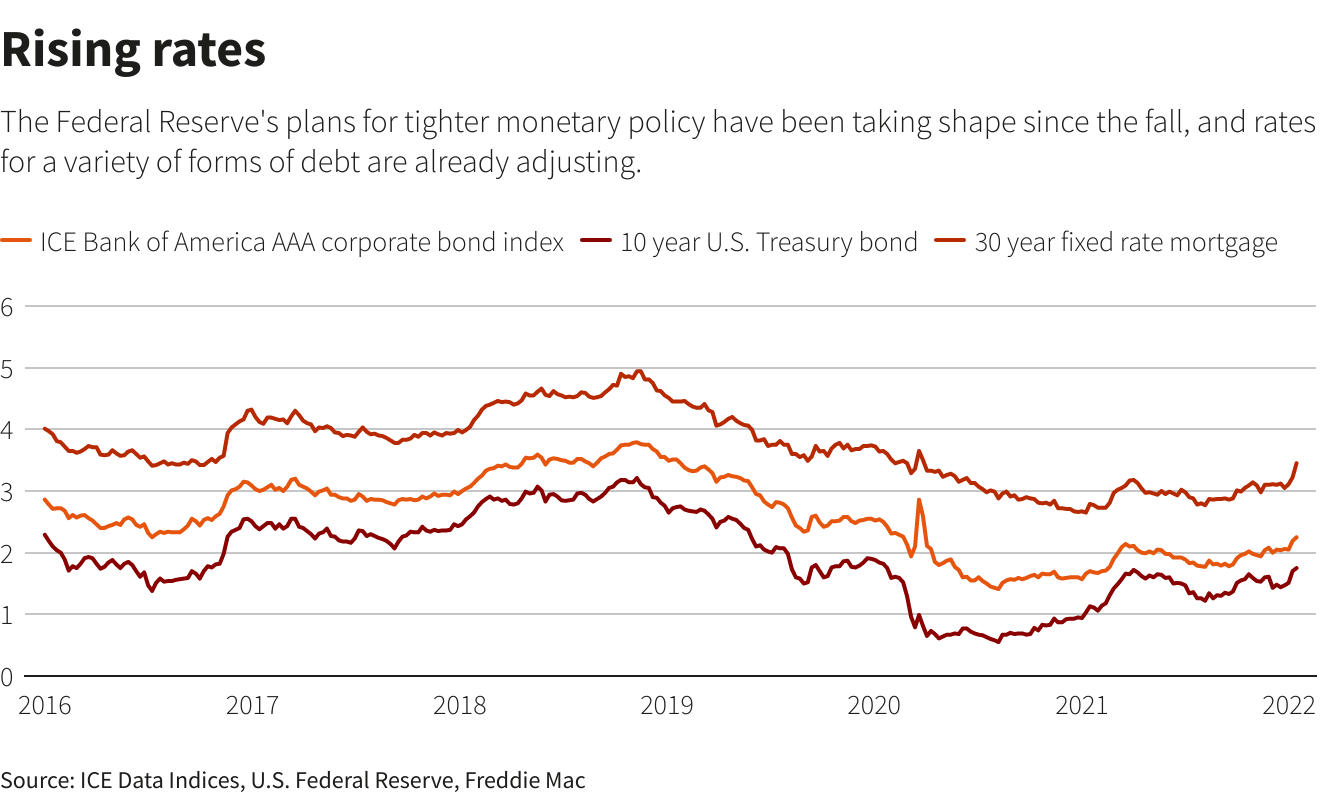

On the basis of comments from Fed officials and the sharp tone of the minutes from the central bank's Dec. 14-15 meeting, interest rates for home mortgages, corporate credit and U.S. Treasury debt are already rising as a result.

Indicators of overall financial conditions - showing how easy or hard it is for households and firms to borrow - have tightened slightly since the Fed began trimming its monthly bond purchases last fall and as the talk around inflation turned more urgent. An estimate of the "shadow" federal funds rate maintained by the Atlanta Fed shows that as of the end of 2021 changes in market interest rates already had produced the equivalent of a 0.6 percentage-point rate hike.

OMICRON DRAG

Still, overall financial conditions remain loose by historic standards. Even if that seems out of step with inflation, there are reasons for the Fed to be reluctant about change coming too fast.

The pandemic continues. While some health officials expect the current outbreak driven by the Omicron variant to subside soon, for now it has slowed hiring and tamped down the economic recovery.

Some economists now predict the U.S. economy will end up having lost jobs in both January and February. That would leave the Fed with the tough choice of raising interest rates in March in the face of declining employment.

Even a temporary Omicron-related "dip" keeps alive concerns that the Fed this year will face not the best, but the worst of both worlds in the form of a slowing economy and inflation that needs even tougher medicine than officials have yet prepared to deliver.

In an interview this month ahead of the Fed's pre-meeting blackout period, Atlanta Fed President Raphael Bostic said the depth of the dilemma turns in part on the degree to which inflation falls on its own, without the need of restrictive Fed policy to force it down through slower growth and slowed employment.

That could happen if, as some economists expect, the virus eases and more workers return to jobs - boosting the supply of goods and services and easing the pace of wage hikes - or if global supply disruptions subside.

There is, however, no guarantee.

Before the onset of the coronavirus, the Fed was struggling against dynamics that kept inflation perennially below its 2% target, and "there is a narrative that says once we are past the pandemic those forces take over so you don't need as aggressive a policy posture," Bostic said. But "none of us going into the pandemic contemplated that inflation would be as high as it is now. So the question really is how forcefully or fulsomely do we have to respond?"

Register now for FREE unlimited access to Reuters.com

Reporting by Howard Schneider; Editing by Dan Burns and Paul Simao

Our Standards: The Thomson Reuters Trust Principles.

Fed tries to match economic risks against market's rush to tighten - Reuters

Read More

No comments:

Post a Comment